Step 2

Identify Harm

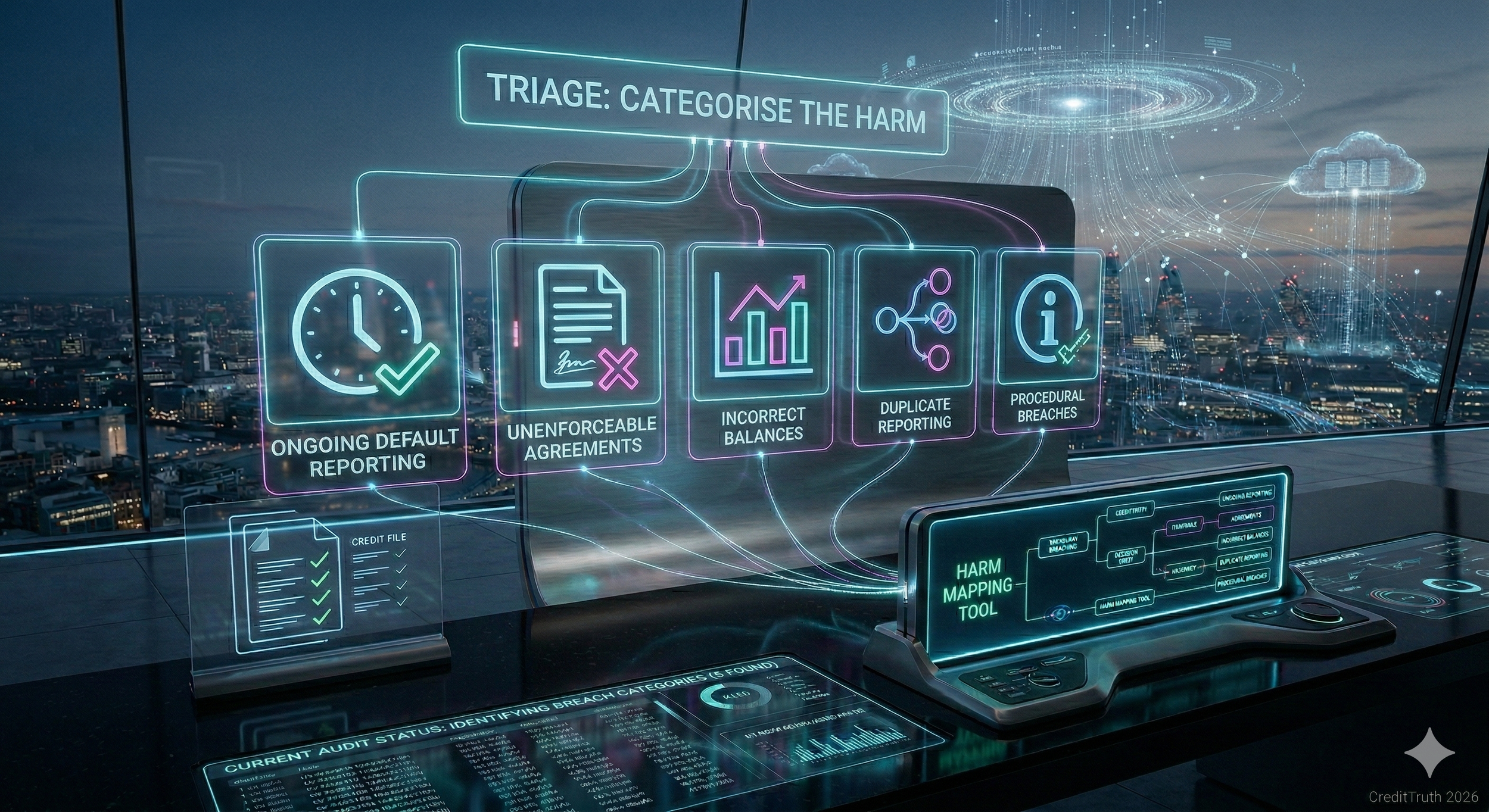

Not all negative data is "correct."

A common myth is that if you owed money and didn't pay it, the negative marker on your file is permanent and legal. This is false. For a entry to remain on your credit file, it must be accurate, timely, and procedurally sound. If the lender has failed any of these tests, the data shouldn't be there. Your job now is to look at your files from Step 1 and see which of these five "Harm Categories" your entries fall into.

1. Ongoing Default Reporting

A default is a "point-in-time" event. It should happen 3–6 months after you first miss a payment.

The Harm: Some lenders keep reporting "Late Payment" markers (1, 2, 3, 4...) for years after they should have defaulted the account. This "drags" the damage forward, making a 2020 debt look like a 2026 problem.

The Lever: We challenge the Default Date to force the entry to age out and disappear sooner.

2. Unenforceable Agreements (CCA 1974)

Under Sections 77–79 of the Consumer Credit Act, you have the right to see the original signed agreement for most credit cards, loans, and store cards.

The Harm: If a debt has been sold multiple times (e.g., to Cabot or Lowell), the paperwork is often lost.

The Lever: If they cannot produce the agreement, the debt is legally unenforceable. They cannot take you to court, and their right to report to credit agencies becomes highly vulnerable.

3. Incorrect Balances & Duplicate Reporting

The Harm: You might see two entries for one debt (one from the original bank and one from a debt collector) both showing a balance. This makes you look twice as indebted as you are.

The Lever: We use SCOR Reporting Principles to demand the removal of "shadow" entries. Your file must reflect reality, not a lender's administrative mess.

4. Selective Reporting ("Data Drift")

The Harm: As we’ve documented in our PayPal Case Study, some lenders only report to one agency (like Equifax) but not others. This is due to become embedded into FCA regulations in 2026 however, GDPR currently applies to this type of negative reporting.

The Lever: If the data isn't reliable enough for all three agencies, it isn't "accurate" under UK GDPR. We challenge the inconsistency to force a total deletion.

5. Procedural Breaches (The "Backdoor" CCJ)

The Harm: A County Court Judgment (CCJ) issued to an address you haven't lived at for years is a "procedural defect."

The Lever: We use the Civil Procedure Rules to "set aside" the judgment. Once the CCJ is set aside, the credit file marker is removed.

"I don’t know which category I’m in yet."

That is perfectly normal. Most cases actually overlap. For example, a debt might be Unenforceable and have an Incorrect Balance.

The goal isn't to be a lawyer; it's to be a Project Manager. By categorising the harm, you stop asking for "mercy" and start pointing out "errors."

The Intimidation Factor - Dealing with Lenders & Debt Collectors

Getting the data is the easy part however, starting to push back on it can feel intimidating. This is often a HUGE deal for a lot of people, especially in 2026 and beyond where the world is a strange place, and life is a large-enough-fight as it is.

It requires strength, mental agility, patience, a removal of emotion, and time. We’ve put together a page that will help with this and give you some anchors to think about.

Next Step

You are now at the critical stage. Before continuing, we are going to talk a bit about The Intimidation Factor.

Now it’s time to move to Step 3: Follow the Process where you can learn how to issue your first formal Notice of Dispute.