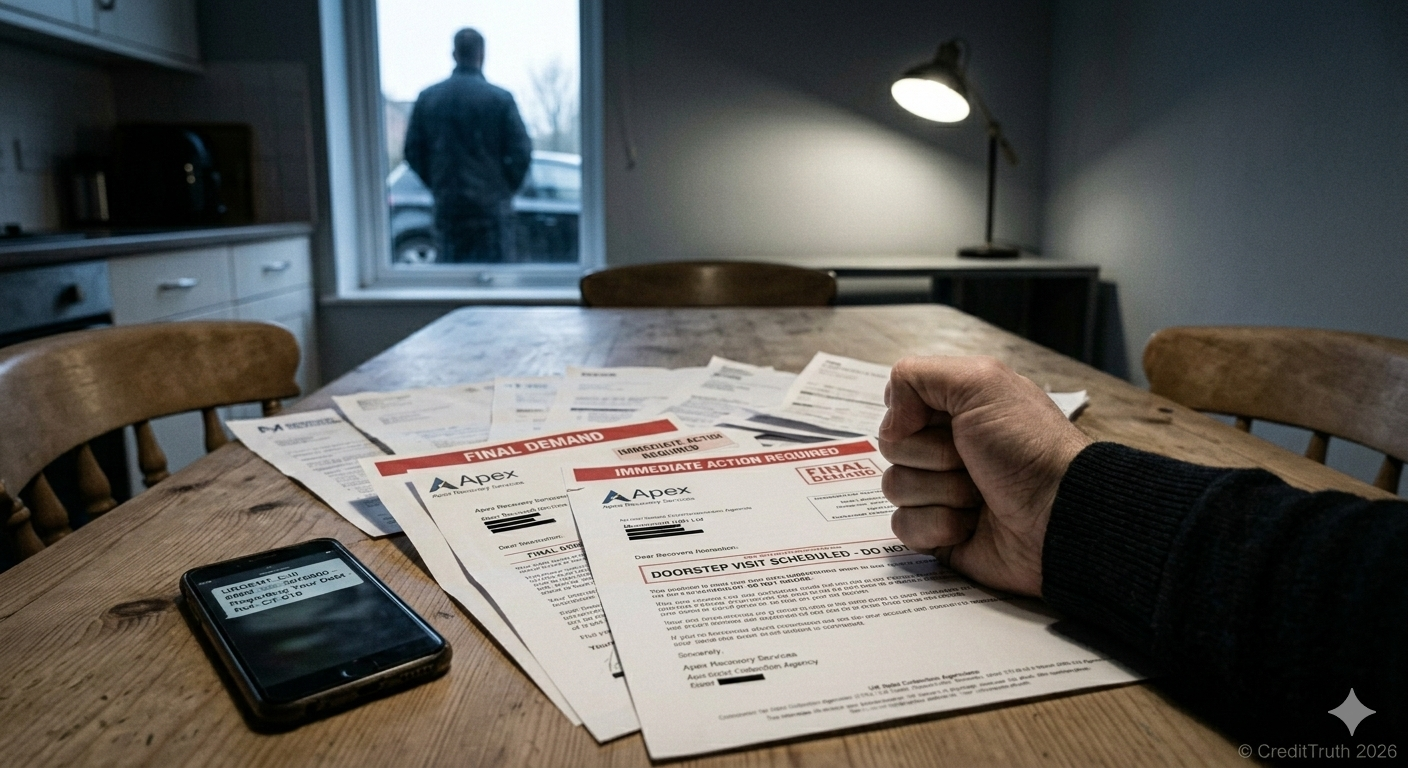

The Intimidation Factor

Dealing with Lenders and Debt Collection Agencies

This is important…

You have the power now.

The most important thing to understand before you send a single letter is this:

The system relies on your anxiety to function.

Lenders, debt collectors, and legal firms spend millions on "Psychological Profiling." They use specific shades of red ink, "Final Notice" headers, and automated phone cycles specifically to make you feel small, isolated, and powerless. If you feel intimidated, that’s okay—it means their marketing is working.

Feeling intimidated is not the same as being defeated.

By being here, you have already broken the cycle. You are moving from a state of "reaction" to a state of clinical tenacity. From this moment forward, you are the Project Manager. You are the one asking the questions. You are the one demanding evidence.

They have the spreadsheets; you have the Statutes. They have the volume; you have the Truth.

Debt is emotional. We know.

You have to decide now that you are going to remove all emotion from your interactions. It’s fine to feel but it’s not fine to project those feelings.

A clinical and non-emotive approach puts you into a position of strength.

A debt collector doesn’t care. They are supposed to care of course under all regulations, but their goal is collection targets and sometimes underhand tactics to get you to pay.

When and if you get to regulatory enforcement yourself, e.g. the Financial Ombudsman Service, they will look at if you have acted as a reasonable complainant. Shouting, screaming, swearing and threatening are all human reactions when you feel threatened yourself however, as hard as it is, (and we know at CreditTruth because we are “gobby,” hate injustice, and we’ve been through it too!)

We promise it’ll stand you in the best stead when you most need it.

Read on for more information to help you.

Authority comes from knowledge, not volume.

When you challenge data on your credit file, you are no longer a "debtor" seeking a favour; you are a consumer enforcing regulatory compliance. The UK financial system is a hierarchy governed by strict rules (FCA CONC, UK GDPR, and the Consumer Credit Act).

If you know these rules better than the person on the other end of the correspondence, the power shift is immediate.

Below is your survival and strategy manual for every level of the escalation ladder.

Level 1: The Original Lenders (Banks & Credit Cards)

High Street lenders (e.g., Vanquis, Capital One, Barclays) are governed by the FCA Handbook, specifically the CONC (Consumer Credit sourcebook) rules.

The Regulatory Lever: Under FCA CONC 7.2, lenders must treat customers in default or arrears with "forbearance and due consideration."

The Strategy: If you entered a Debt Management Plan (DMP) or notified the lender of financial distress, but they applied a default marker months after the relationship broke down, they have breached the Principles of Data Accuracy.

The Posture: Argue the Timeline, not the money. A default applied late stays on your file for too long. Demand they "re-age" the entry to the date the relationship actually failed.

The Commercial Reality: Remind them that a generic "computer says no" response leads to a Financial Ombudsman Service (FOS) case. This costs the lender a mandatory £650 case fee regardless of the outcome. Often, correcting your data is the only rational business decision for them.

Level 2: Debt Collection Agencies (DCAs)

Purchasers like Cabot, PRA Group, or Lowell buy debts in bulk. They rely on "Information Asymmetry"—the hope that you don't know your statutory rights.

The Statute Barred Defense (The 6-Year Rule): Under the Limitation Act 1980, a creditor generally has 6 years (5 years in Scotland) to take legal action.

The Trigger: The clock starts from your last payment or written acknowledgement.

The Strategy: Do not make a token payment on an old debt; this "resets" the clock. If the debt is statute-barred, they cannot legally sue you. Demanding payment for a statute-barred debt after being notified of its status is a breach of FCA CONC 7.15.

The Section 77-79 CCA Request: If the debt is active, demand a "True Copy" of the original credit agreement.

The Rule: If they cannot provide this within 12 working days, the debt is legally unenforceable.

The Posture: "Close is not compliant." If the documents are missing or reconstituted incorrectly, the debt cannot be enforced in court.

Managing Intimidation: DCAs use "Urgency Tactics" (red ink, "Doorstep Visit" threats).

The Fact: A debt collector is a private citizen with zero legal right of entry to your home.

The Response: Send a "Notice of Communication Preference" stating you will only deal with them in writing. This stops the harassment and creates a clinical paper trail.

Level 3: The County Court Process (Legal Action)

If a firm like BW Legal issues a County Court Claim (an N1 form), do not ignore it. A CCJ is the most damaging marker a file can have, but it is also a process full of "Trapdoors" for the lender.

Beyond "Bad Service": While serving papers to an old address allows you to "Set Aside" a judgment, there are deeper technical defenses:

Notice of Assignment: Under the Law of Property Act 1925, you must be formally notified when a debt is sold. No notice = no legal right to sue.

Default Notice Failures: Before terminating an agreement, a lender must send a valid Default Notice under Section 87(1) of the CCA 1974. If the notice is missing, or the format is flawed, the claim is procedurally void.

Balance Derivation: We demand a full breakdown of the balance (a CPR 31.14 request). If they cannot prove how a £500 debt became a £3,000 claim, they cannot evidence their loss to a judge.

The Strategy: Filing a contested defense moves your file from the "Automation" pile to a "Legal Review." Many DCAs will drop a claim rather than pay a solicitor to argue a flawed case.

Level 4: Bailiffs & Enforcement Agents

This is the highest pressure stage. You must know the difference between a Bailiff and a Debt Collector.

The Golden Rule: Keep your doors and windows locked.

A Bailiff (Enforcement Agent) has a court warrant, but in almost all consumer debt cases, they cannot force entry. They can only enter through an "open or unlocked" door.

The Strategy: You can negotiate a "Controlled Goods Agreement" to pay in instalments without letting them in. They cannot seize "essential household items" (cooker, fridge, beds) or "tools of your trade" (up to £1,350).

The Stay of Execution: Even at this stage, you can apply to the court (Form N245) to stop the bailiffs and set a monthly payment you can actually afford.

Why You Will Succeed

The system is built on the assumption that you will be too overwhelmed to look at the rules. By becoming a Project Manager of your own data, you become "High Friction."

Lenders and collectors hate friction. It costs them time, money, and regulatory standing. When you show them you know your rights, you move from being a "target" to being a "liability" they would rather resolve than fight.

Strength is not about being loud; it is about being correct.