Step 3

Follow the Process

Execution is everything.

You have audited your files and identified the harm. Now, you must engage the system. The biggest mistake people make at this stage is being "emotional" in their correspondence. Lenders and Debt Collection Agencies (DCAs) have departments dedicated to filtering out emotional pleas. They do not, however, have a filter for Formal Regulatory Disputes.

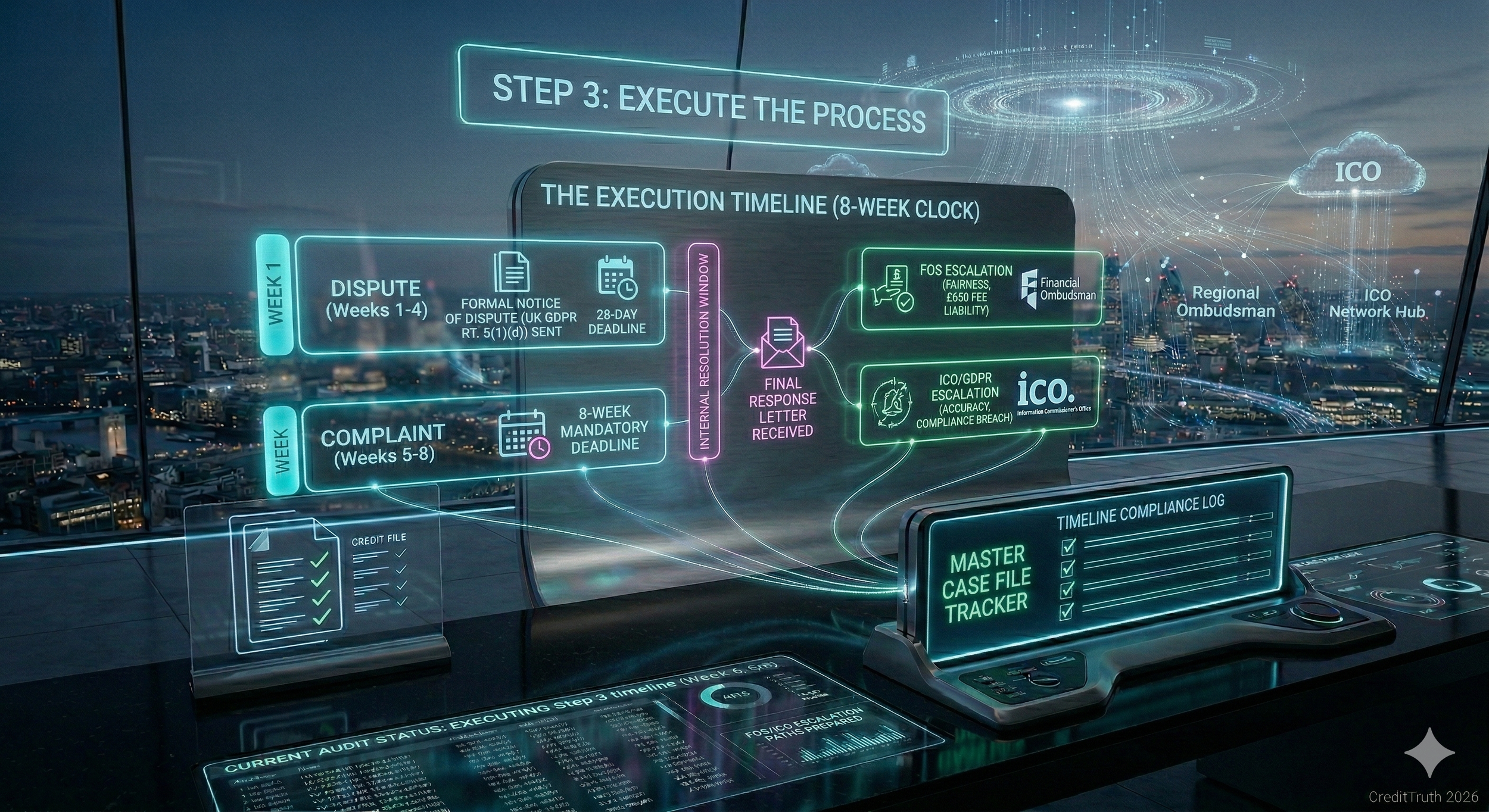

To win, you must follow a rigid, 3-stage process. This ensures that if the lender refuses to correct the data, you have a perfect "Evidence Pack" ready for the Financial Ombudsman Service (FOS) or the Information Commissioners Office (ICO).

Stage 1: The Formal Notice of Dispute

Do not send a "letter of complaint" yet. Start with a Formal Notice of Dispute. This is a short, clinical document that puts the firm on notice that you are challenging the accuracy or the lawfulness of their data processing.

The Content: State clearly what the error is (e.g., "The default date is incorrect" or "The agreement is unenforceable").

The Request: Ask for the specific evidence they rely on to justify the entry (e.g., the original CCA agreement or the contemporaneous Default Notice).

The Deadline: Give them 28 days to respond. This aligns with the UK GDPR "Right to Rectification" timelines.

Pro-Tip: If you are dealing with a DCA, this is where you also include your Section 77-79 CCA Request and the £1 statutory fee. This legally "pauses" their ability to collect.

Stage 2: The Final Response (The 8-Week Clock)

If the firm rejects your dispute or ignores it, you must trigger a Formal Complaint. This starts a mandatory 8-week countdown.

The Goal: You aren't necessarily expecting them to agree with you. You are "exhausting their internal process."

The Lever: Under FCA DISP rules, they must send you a "Final Response Letter" within 8 weeks. This letter is your "Golden Ticket"—without it, you cannot easily move to the next stage.

The Strategy: If they haven't solved the issue by Week 8, do not keep arguing with them. The conversation with the lender is now over.

Stage 3: Independent Escalation (The "Kill-Shot")

This is where the power fully shifts. Once you have a Final Response (or the 8 weeks have passed), you take your evidence to the regulators.

Financial Ombudsman Service (FOS): Use this for "Fairness" issues. If a lender treated you poorly, ignored your DMP, or applied a late default, the FOS can order them to remove the entry and pay you compensation for distress.

Commercial Reality: Remember, this costs them £650 just for being investigated.

Information Commissioner’s Office (ICO): Use this for "Data Accuracy" issues. If a lender is reporting a debt they can't prove exists, or reporting to one agency but not others, the ICO is the enforcement body for UK GDPR.

The Court (N244 Set Aside): If you are dealing with a CCJ, this is the stage where you file your court papers to have the judgment vacated.

The Three Rules of the Process

To maintain your position of strength, you must adhere to these rules throughout the 3 stages:

Keep a Contemporaneous Evidence Log: Record the date of every letter sent and received. Screenshot every update on your credit file. At CreditTruth, we call this the "Master Case File."

Writing Only: Never, under any circumstances, "hop on a call" to discuss your dispute. If it isn’t in writing, it didn’t happen. If they call you, hang up and send a template email reminding them of your communication preference.

Don't Blink: DCAs will often send a "settlement offer" midway through this process. If your goal is deletion, do not pay until the correction is confirmed in writing. Paying a flawed entry "satisfies" it, but it doesn't remove the damage.

Ready to Start?

The process begins with the first letter.

Before diving in, check out Step 4 which gives you useful information on tracking and maintaining visibility over your complaints.

You’ll also find a link to our Document Hub, where you can download the specific "Notice of Dispute" for your category of harm.